If you sell anything across borders, USDT is probably already in your customers' wallets. Tether has a market cap of roughly $186 billion as of June 2026, holds around 59% of the stablecoin sector, and, for a few hours in early June, even edged past Ethereum to become the second-largest crypto asset.

For a merchant, that scale means one thing: a USDT payment gateway is the path of least resistance into crypto payments.

This guide covers how to accept USDT, which settlement network to use, and where the trade-offs lie.

Why do businesses accept USDT in 2026?

Because it behaves like a dollar but moves like crypto, USDT is pegged 1:1 to the US dollar, so a $500 invoice settles as $500 regardless of what Bitcoin does that afternoon. That removes the single biggest objection merchants have to crypto.

The practical wins stack up fast. Cross-border settlement that costs $25–50 and takes days over SWIFT drops to cents and seconds on-chain.

There are no chargebacks – blockchain transfers are final, which matters enormously for digital goods, iGaming, and forex. And you reach a customer base that already transacts in stablecoins.

Per Eco, if you're sending dollars on-chain, roughly 7 out of 10 times the token is USDT – it dominates the stablecoin transfer share.

For operators serving Argentina, Turkey, Nigeria, or Southeast Asia, it's often the only dollar rail customers actually use.

What is a USDT payment gateway, and how does it work?

A USDT payment gateway is the infrastructure that lets your business accept Tether and turn it into something usable – a stablecoin balance, fiat in your bank, or another crypto.

It's not the same as pasting a wallet address into the checkout.

A raw wallet gives you an address and nothing else. A gateway generates a unique address per invoice, watches the blockchain for the transfer, confirms the amount, flags underpayments, and pushes a webhook the moment funds land.

The flow in four steps:

- The customer picks USDT at checkout and selects the network they want to pay on.

- The gateway issues a unique invoice – a one-time address and exact amount, with a payment window.

- The customer sends funds from any compatible wallet or exchange.

- Funds arrive and settle, often within seconds. With auto-conversion on, incoming USDT settles straight to your preferred stablecoin.

0xProcessing runs this on its own node infrastructure rather than third-party aggregators, which keeps confirmation fast and acceptance near 99.9%.

USDT networks and fees: TRC-20 vs ERC-20 vs BEP-20 vs Solana

This decision quietly determines your cost per transaction. The same USDT costs wildly different amounts to move across chains.

A snapshot from June 2026:

| Network | Standard | Typical fee | Speed | Best for |

|---|---|---|---|---|

| Tron | TRC-20 | ~$0.20–$1 (staked); $1–5 burning TRX | ~3 sec | High-volume consumer payments |

| Solana | SPL | ~$0.0003 | <1 sec | Fast retail, micro-payments |

| BNB Chain | BEP-20 | ~$0.02–0.05 | Seconds | Low-cost retail |

| Polygon | – | ~$0.01 | Seconds | Cost-efficient payouts |

| Ethereum | ERC-20 | ~$0.05–0.10 normal; $1–3 peaks | Minutes | Institutional, DeFi, bank/OTC |

The "$30 Ethereum gas" figure in older guides is a 2021–2022 artifact. Per

Etherscan, average gas ran around 0.3–0.6 gwei through mid-2026, putting a normal ERC-20 transfer at five to ten cents.

Which network should you choose?

Pick by who's paying you.

Want to accept crypto payments on your website?

For consumer-facing volume – iGaming deposits, retail, remittance corridors – Tron (TRC-20) is the default. It carries roughly half of the USDT supply, settles in 3 seconds, and is supported by every exchange. For speed and near-free retail, Solana is hard to beat. Reserve Ethereum (ERC-20) for when a counterparty specifically requires L1.

A good gateway lets you connect across several networks at once. 0xProcessing supports USDT across 18 blockchains, including all networks listed above.

USDT vs USDC: which stablecoin should you accept?

Both are dollar-pegged, but they split on the trust model and regulation.

USDT has deeper liquidity and wider exchange support, especially on Tron; USDC leans on fuller reserve transparency and is the compliant default on regulated EU venues under MiCA. Most merchants accept both and let the customer choose. For the full breakdown, see our USDT vs USDC comparison.

How to accept USDT payments: step-by-step

Knowing how to accept USDT payments comes down to five steps, more administrative than technical. Zero to live:

- Register a merchant account. Sign up with the gateway and provide basic business details.

- Pass KYB. Company documents, beneficial ownership, and the standard onboarding. For regulated high-risk verticals, this is where a specialist processor earns its keep, because the AML logic is built for your vertical.

- Choose networks and settlement. Decide which USDT networks to accept, and whether to auto-convert incoming funds to a single stablecoin.

- Integrate via API, payment link, button, or invoice flow.

- Test, then go live. Run a small transaction on each network, confirm the webhook fires, then switch on real traffic.

Most merchants go live within a week; guided onboarding for high-risk accounts runs 3–7 days.

Want a transparent setup for your volume? 0xProcessing onboards merchants across 85+ coins and 18 blockchains, with VRCS (Volatility Risk Control System) auto-conversion and 0% withdrawal fees.

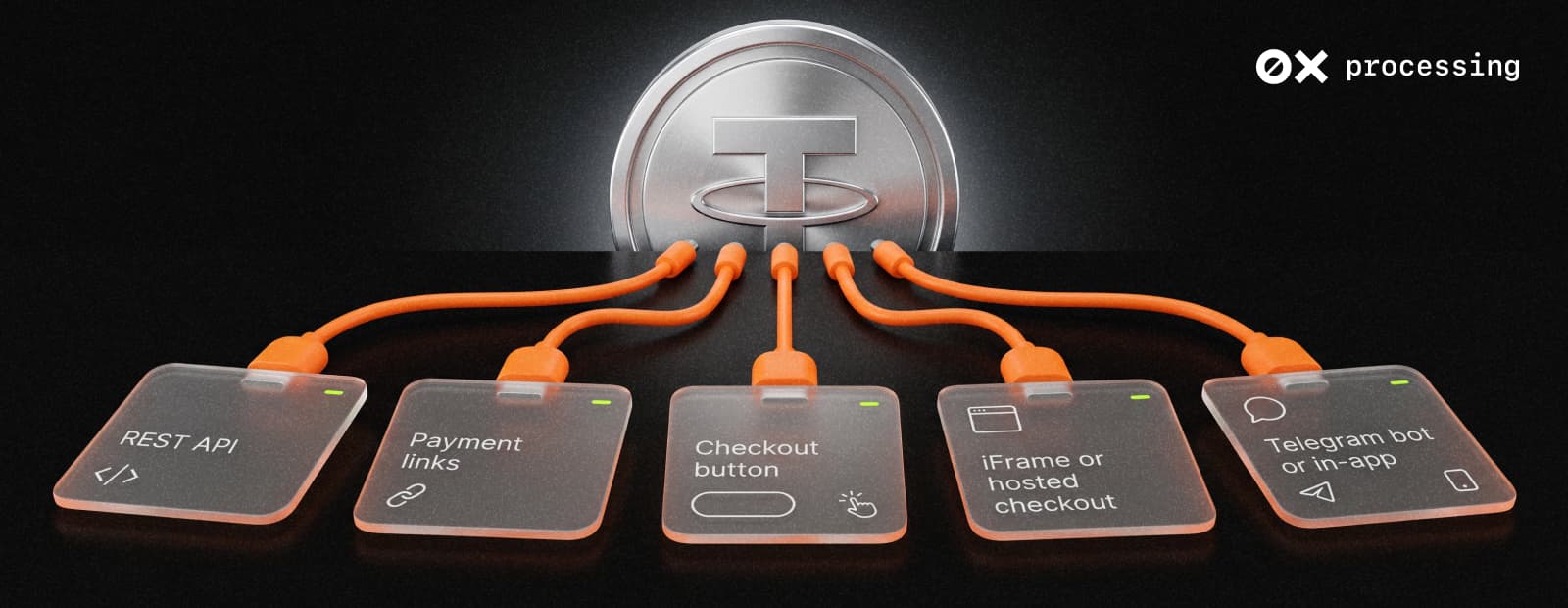

Get startedWhat integration options exist for accepting USDT?

There are two broad routes: ready-made CMS plugins or a flexible custom integration.

Plugins for platforms like Shopify, WooCommerce, and Magento install in minutes with little code, but trade control for convenience. Beyond plugins, these are the main paths.

REST API

The most flexible option. Generate invoices programmatically and listen for webhook callbacks – the backbone of high-volume and automated setups.

Payment links

No site required. Generate a link, send it over email or chat, and get paid. Ideal for invoicing and social-media sales.

Checkout button

A hosted button you embed with minimal code, adding USDT to an existing page.

iFrame or hosted checkout

Embed the payment form directly, or redirect to a hosted page that handles the flow.

Telegram bot or in-app

For businesses operating within messaging channels, payments are processed via a bot or an in-app flow.

0xProcessing offers these flexible paths rather than off-the-shelf plugins, plus white-label forms you can brand as your own.

It's a custodial gateway by design – a feature for the regulated verticals it serves. Unlike a non-custodial wallet, where you hold the keys and the compliance burden, a custodial gateway manages settlement, screening, and blockchain confirmation for you.

Pros and cons of accepting USDT

Pros

- Dollar stability without leaving crypto rails.

- Low fees on the right network – cents, not the 2.9% + $0.30 of cards.

- No chargebacks – final settlement protects high-risk merchants.

- Global reach into markets where stablecoins are the default dollar.

- Fast settlement – seconds on Tron or Solana versus days on a wire.

Cons

- USDT is centralized. Tether Limited can freeze tokens – over $4.4 billion frozen in total as of 2026 across 65+ countries (roughly $3.5 billion of it since 2023). Not a reason to avoid USDT, but a reason to settle quickly and not park large balances on-chain.

- Network confusion. Customers occasionally send to the wrong chain. A gateway showing the correct address per network reduces this.

- Regulatory drag in the EU under MiCA (more below).

How do you choose a USDT payment processor?

Once you've decided to accept Tether, the shortlist comes down to a few questions. If two or more answers are blank, you're not ready to sign.

- Which USDT networks do my customers use, and does the processor support all of them?

- What's the all-in rate at my volume, not just the headline base fee?

- Is settlement custodial or non-custodial, and does that fit my risk posture?

- Does it auto-convert to a stablecoin or fiat to neutralize freeze and accounting exposure?

- What's the off-ramp and its cost – free SEPA, or a $25–50 SWIFT wire?

- How long does onboarding take, and which KYB documents are required?

- Does the licensing cover my jurisdiction and vertical?

- Are there withdrawal minimums that trap funds on the platform?

The headline fee rarely bites later – the off-ramp cost, onboarding delay, or a missing network usually does.

Converting USDT to fiat and withdrawing to a bank account

Receiving USDT is half the job. Getting it into your operating account is the other half.

Most processors let you keep the USDT, swap it, or off-ramp to fiat. The rails matter: SWIFT wires run $25–50 and take a few days; SEPA in the EU is typically free; instant rails like PIX or UPI settle near-instantly at near-zero cost.

Volatility isn't a concern for USDT itself. The bigger question is freeze and exposure risk, which is where auto-conversion helps – settling incoming funds to a single managed stablecoin keeps your balance clean.

0xProcessing's VRCS (Volatility Risk Control System) handles this at the moment of payment with no extra fee, with SWIFT/SEPA off-ramp and bank settlement in 3–5 working days. For the broader picture, see our guide on accepting stablecoin payments.

Is accepting USDT legal? Regulation by region

The 2026 picture is clearer than ever – stablecoins have moved from the grey zone to a regulated payment instrument across most major markets.

United StatesThe GENIUS Act, signed in July 2025, created the first federal framework for payment stablecoins, with final rules targeted for July 2026 and the law effective no later than January 2027.

It regulates issuers, not merchants – you can accept and hold USDT freely.

EUMiCA is fully in force, with a hard deadline of July 1, 2026, for issuers and service providers. On regulated EU venues, USDT has effectively been pushed out rather than merely narrowed – several platforms now flag that it no longer meets regulatory requirements and steer EU users toward USDC, which remains the compliant option. Self-custody and direct acceptance sit outside the tightest constraints (a merchant taking USDT into self-custody isn't a CASP). Still, EU-facing businesses should plan around USDC as the regulated default. A licensed processor handles this compliance layer for you.

UKThe FCA is finalizing its regime under the Financial Services and Markets Act 2023, converging on licensed issuers, reserve backing, and AML.

SingaporeMAS requires 100% reserves and redemption at par within five business days – clear and merchant-friendly.

The throughline: regulators target issuers and custodians, not the businesses accepting stablecoins.

How are USDT payments taxed and accounted for?

Lighter than volatile crypto, but not zero. Because USDT holds a stable $1 value, there's little capital gain or loss between receipt and conversion – the headache that makes BTC or ETH accounting painful. In most jurisdictions, incoming USDT still counts as taxable business revenue at its dollar value on the day it is received, and a gateway's transaction-level records make it straightforward to report. Settling on a single stablecoin keeps the books clean and the audit trail simple. Confirm specifics with a local advisor.

Best industries for USDT payments

The strongest cases share a profile: cross-border, high-volume, or chargeback-sensitive. Cross-border trade skips the correspondent-banking chain. E-commerce in emerging markets with low card penetration. iGaming and betting – fast deposits, instant payouts, no chargebacks. Forex and trading platforms – dollar balances without a bank. SaaS – recurring billing in a stable unit. See who already accepts Tether for real examples. On cost, the comparison usually closes the decision. Card acquiring runs about 2.9% + $0.30, plus 1–3% cross-border, so an international card payment can cost 4–6% all-in. USDT on Tron or Solana costs a few cents plus your processor's fee. On a $100K monthly volume, that gap is real money.

How to start accepting USDT with 0xProcessing

The setup is the easy part.

For USDT processing at scale, 0xProcessing supports Tether across every major network – TRC-20, ERC-20, BEP-20, Solana, Polygon, and more – with auto-conversion via VRCS (Volatility Risk Control System), 0% withdrawal fees, and mass payouts. The platform has been live since 2020, has undergone four external audits (2022–2025), and runs on its own node infrastructure with real-time AML/KYT.

Ready to accept Tether? Settle across 85+ coins and 18 blockchains, with stablecoin auto-conversion included and 0% on withdrawals and payouts.

Start accepting USDTBottom line

USDT is the most pragmatic entry point into crypto payments in 2026 – dollar-stable, deeply liquid, and accepted everywhere your customers already transact.

The decisions that matter aren't whether to accept it, but which networks to settle on and how fast you convert.

Get those right, and you've cut cross-border costs by an order of magnitude while eliminating chargebacks.

FAQ

How do I accept USDT payments for my business?

Register with a USDT payment gateway, pass business verification (KYB), choose which networks to accept, integrate via API or a payment link, then test and go live. Most merchants are processing within a week.

Do I need KYC to accept USDT?

For a regulated custodial gateway, business verification (KYB) is standard: company documents and beneficial ownership. Requirements vary by provider and vertical, but a licensed processor handles AML/KYT screening so you stay compliant.

Which USDT network is cheapest to accept?

Solana (~$0.0003) and BNB Chain (~$0.02) are the cheapest, with Tron (TRC-20) the most widely used at roughly $0.20–1 with staked energy. Reserve Ethereum ERC-20 for counterparties that require it.

Can I convert USDT to fiat automatically?

Yes. Auto-conversion settles incoming USDT into a stablecoin or fiat at the time of payment. 0xProcessing's VRCS (Volatility Risk Control System) does this with no extra fee, with SWIFT/SEPA off-ramp in 3–5 working days.

What happens if a customer underpays?

The gateway flags it as a partial payment and notifies both sides. You can accept, reject, or hold it for review. A unique address per invoice is what makes this detection reliable.

Is accepting USDT legal?

In most major markets, yes. The US GENIUS Act, EU MiCA, UK FCA rules, and Singapore's MAS framework regulate stablecoin issuers, not the merchants accepting them.