How can you transfer crypto revenue to a corporate bank account efficiently and with minimal losses? In 2026, the optimal off-ramp strategy is a two-stage process: first, instant conversion to stablecoins (USDT/USDC) to hedge against volatility, then withdrawal via integrated payment solutions with virtual IBANs or trusted partner networks. This reduces costs from the traditional 3–6% for SWIFT transfers to 1–1.5%, whilst maintaining compliance with regulatory requirements.

In this article, you will find:

- a definition of an off-ramp and an explanation of its importance for international business;

- a comparison of withdrawal methods (exchanges, P2P, payment gateways);

- an analysis of the role of stablecoins as a key tool for 2026;

- an overview of regional specifics for Europe, Asia, the US and the Middle East;

- practical recommendations for minimising risks and fees.

Get a step-by-step guide: how to convert cryptocurrency or withdraw USDT to a bank account without unnecessary losses.

What is a crypto off-ramp and why is it complicated

A crypto off-ramp is the process of converting cryptocurrency into fiat currency (dollars, euros, pounds, dirhams) and withdrawing it to a traditional bank account. At first glance, the task seems simple, but in practice, international businesses face a number of serious challenges.

Key challenges:

- High fees. Traditional SWIFT transfers via correspondent banks can eat up between 3% and 10% of the transfer amount, particularly for cross-border transactions. Furthermore, banks often apply unfavourable exchange rates, adding a hidden 1–2% on top of the official rate.

- Slowness. Bank transfers only operate on working days and during business hours. A SWIFT transfer can take between 3 and 7 working days. For businesses with high cash flow turnover, this is critical.

- Regulatory restrictions. Many banks remain suspicious of crypto companies and may freeze accounts or return payments without explanation. By 2026, the situation improves, but problems remain.

- Volatility during the transfer. If you have sold cryptocurrency and are waiting for the funds to be credited for 3–5 days, the exchange rate may change by 5–10%, and the actual amount in fiat currency will turn out to be quite different from what you expected.

- Liquidity fragmentation. Different exchanges and services offer different rates and fees, and funds may be scattered across several platforms.

2026 statistics. Stablecoins have become the primary tool for mitigating volatility on the path to fiat, acting as the ideal bridge before the final withdrawal. Their total supply is approaching $320 billion, and the share of transactions using stablecoins in the total volume of on-chain transfers continues to grow. Institutional capital now forms long-term liquidity, and companies are seeking reliable, regulated withdrawal methods.

Main off-ramp methods: pros and cons

The main crypto off-ramp solutions remain specialised exchanges, direct transfers and payment gateways.

Centralised exchanges (Binance, Coinbase, Kraken, Bybit)

Large centralised exchanges remain the most common method of withdrawing funds, especially for companies that are already actively trading on them.

How it works. You sell cryptocurrency on the exchange (paired with USD, EUR or another fiat currency), after which you initiate a fiat withdrawal to your corporate bank account via SEPA (for euros), SWIFT (for international transfers) or ACH (for the US).

Pros:

- High liquidity – you can sell large amounts without significantly affecting the price.

- Relative simplicity – a familiar interface for most crypto users.

- A wide choice of currencies and withdrawal destinations.

- Regulated platforms with KYC/AML procedures.

Cons:

- Fees: 0.1–0.5% for trading + a fixed withdrawal fee (from $1 to $50 depending on the currency and amount).

- Delays: withdrawals to a bank account can take 1–3 working days.

- Risk of the exchange freezing your account in the event of suspicious transactions.

- Requirement to undergo verification and provide documents.

P2P platforms (Binance P2P, Bybit P2P, OKX P2P, LocalCoinSwap)

P2P platforms connect buyers and sellers directly, allowing you to convert crypto to fiat by choosing the exchange rate and transaction options.

Want to accept crypto payments on your website?

How works decentralized off-ramps

You place an order to sell cryptocurrency at your desired rate, find a buyer, and transfer the crypto bank account or via another method once payment confirmation is received.

Pros:

- Often a better rate than on exchanges (negotiable).

- Accessible in regions with restrictions on bank transfers.

- Flexible payment methods (local banks, e-wallets).

- Opportunity to trade with verified counterparties (ratings, history).

Disadvantages:

- Risk of fraud (although platforms offer escrow services).

- Slower than exchanges – you need to find a counterparty and negotiate.

- Requires more manual effort, difficult to automate.

- Transaction limits for new sellers.

P2P dominates in Latin America, and some countries in Asia and Africa, where access to international bank transfers is limited.

Payment gateways and specialised services (0xProcessing and others)

Crypto withdrawal best practices for businesses, which integrate directly via API and automate the entire withdrawal process.

How it works. You connect the gateway to your website or internal system. When a withdrawal is required, funds are automatically converted into stablecoins or fiat and sent to your bank account or virtual IBAN.

Pros:

- Full automation – no need to manually withdraw from each exchange

- Speed: minutes, not days (thanks to the use of stablecoins as a bridge).

- A single interface for all operations (receipt, conversion, withdrawal).

- Built-in compliance and AML checks.

- Ability to set up automatic rules (e.g., withdraw when a certain balance is reached).

Cons:

- Integration required (although APIs are usually straightforward).

- Not available everywhere (depends on the partner network in a specific region).

- Fees may be higher than those on exchanges, but lower than bank charges.

Decentralised off-ramps

With the development of DeFi and stablecoins, decentralised off-ramps are emerging for withdrawing to fiat via stablecoin off-ramping and partner networks.

How it works. You use a DeFi protocol to convert to a stablecoin, then withdraw to a bank card or account via a partner service.

Pros:

- Non-custodial – you control your keys right up to the last moment.

- Global access with no restrictions.

- Innovative solutions with low fees.

Cons:

- Complexity for non-crypto users.

- High gas fees on the mainnet (L2 can be used).

- Limited liquidity for large amounts.

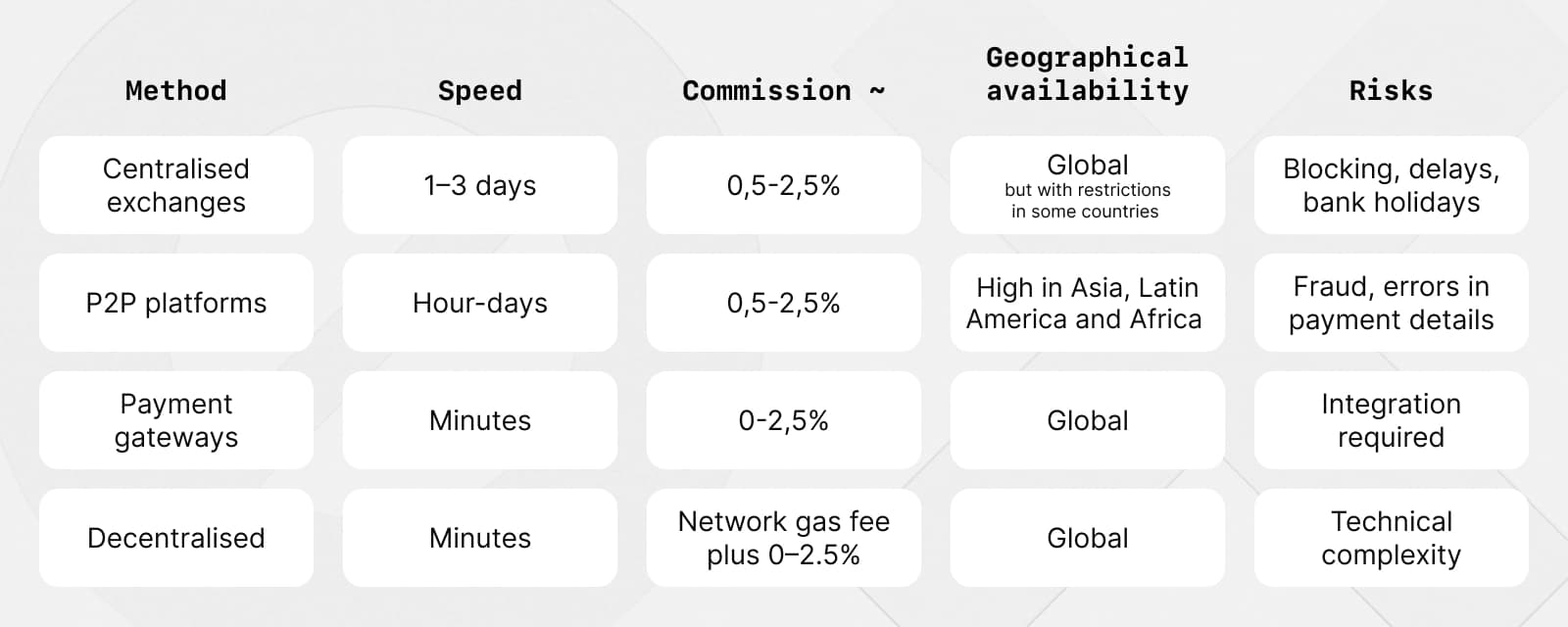

Comparison of off-ramp methods: a selection table

| Method | Speed | Commission (approximate) | Geographical availability | Risks | Who is it for |

|---|---|---|---|---|---|

| Centralised exchanges | 1–3 days | 0,5-2,5% | Global, but with restrictions in some countries | Blocking, delays, bank holidays | Companies already working with exchanges |

| P2P platforms | Hour-days | 0,5-2,5% | High in Asia, Latin America and Africa | Fraud, errors in payment details | Small amounts, regions with banking sector restrictions |

| Payment gateways | Minutes | 0-2,5% | Global | Integration required | Professional businesses with regular withdrawals |

| Decentralised | Minutes | Network gas fee plus 0–2.5% | Global | Technical complexity | Projects focused on cryptocurrency and DeFi |

Regardless of which off-ramp method you choose, a key element of a modern strategy is the use of stablecoins as a stable bridge between cryptocurrency and fiat. 0xProcessing offers a professional solution for businesses:

- accept payments in 65+ cryptocurrencies;

- automatically convert to USDT via VRCS (volatility protection);

- withdraw funds via our partner network with virtual IBANs in Europe, Asia and the Middle East.

API integration allows you to fully automate the process and forget about manual withdrawals from exchanges.

The role of stablecoins in modern off-ramps

Stablecoin off-ramping has become the primary tool for mitigating volatility and building effective strategies. By 2026, they will serve as a "digital dollar on the blockchain", which can be transferred instantly and at minimal cost.

Why stablecoins are important:

- Exchange rate pegging. As soon as you receive a payment in a volatile cryptocurrency (BTC, ETH), instant conversion to a stablecoin protects you from a price drop in the following minutes or hours.

- Transfer speed. Transferring USDT or USDC between exchanges, wallets and services takes minutes, especially on TRC-20, BEP-20 networks or L2 solutions. This allows you to aggregate liquidity and choose the best moment for the final withdrawal.

- A single bridge. Instead of holding balances across a dozen exchanges in different currencies, you can consolidate everything into stablecoins in a single wallet and withdraw via the optimal channel.

- 24/7 availability. Stablecoins are not subject to bank holidays or weekends. You can lock in profits and prepare funds for withdrawal at any time.

- Liquidity. The total supply of stablecoins is approaching $320 billion, and they are accepted by all major exchanges and off-ramp services.

The use of stablecoins for transactions is growing faster than for simple storage. Institutional players are increasingly using them as the primary tool for moving capital between exchanges and jurisdictions.

Regional features of withdrawals: a comparative table

| Region | Key payment systems | Withdrawal speed | Tax considerations | Regulatory environment | Suitable for |

|---|---|---|---|---|---|

| Europe | SEPA Instant, virtual IBANs | Seconds (SEPA Instant) | Conversion is a taxable event. In Germany: 0% capital gains tax (CGT) if held for more than one year | MiCA (from 2025) – high certainty | Companies seeking speed and transparency; long-term investors |

| USA | ACH, partner banking networks | 1–3 days (ACH) | Each sale is a taxable event | Complex, state-level regulation (BitLicense in New York) | Large businesses with a local presence |

| Singapore | Virtual IBANs, a well-developed banking system | Hour-days | 0% capital gains tax | Friendly, transparent | Holding companies and fintech firms |

| Hong Kong | Licensed exchanges, institutional platforms | Hour-days | Depends on the structure | Licensing of crypto platforms | Institutional investors seeking access to Asian capital |

| UAE | Partner networks, direct withdrawals | 24-48 hours | 0% personal income tax, 0% CGT | VARA, ADGM – transparent rules | International holding companies and family offices |

| Asia | P2P platforms, local banking partnerships | Hour-days | Depends on the country | Emerging | Businesses with a local presence, small amounts |

Real-world business cases

The problem. A SaaS platform with subscriptions priced in euros was accepting cryptocurrency payments from international customers. Manually withdrawing funds from exchanges and converting them was taking up the finance team’s time, and volatility was sometimes eroding profits.

Solution. Setting up an automatic off-ramp via API. Cryptocurrency payments are instantly converted to USDT, and when the €10,000 threshold is reached, they are automatically withdrawn to a euro account.

Result. Full process automation, reduced costs, protection against volatility.

Risks when withdrawing funds and how to minimise them

Corporate crypto conversion can involve several risks. Here are the main ones.

Risk 1: Account freeze on an exchange

Exchanges may freeze an account on suspicion of a rule violation or at the request of regulators. Funds may be inaccessible for weeks or months.

Solution – diversify your platforms. Do not keep all your assets on a single exchange. Use several trusted platforms and withdraw large sums regularly.

Risk 2: Volatility during transfer

While you wait for the funds to be credited to your bank account, the exchange rate may change, and you will lose part of your profit.

Solution – use stablecoins as an intermediate step. Lock in the exchange rate instantly and plan the withdrawal separately.

Risk 3: Regulatory restrictions and account freezes

Banks may refuse to credit funds or freeze an account if they deem the transaction suspicious.

Solution – work only with licensed partners who understand the specifics of the crypto business. Provide a full set of documents and be prepared to explain the origin of the funds. Use jurisdictions with crypto-friendly regulations (UAE, Singapore).

Risk 4: High fees

Choosing the wrong method can cost 5–10% of the amount.

Solution – compare fees; use the table above. For large sums, negotiate individual terms.

Risk 5: Fraud on P2P

When dealing directly with unknown counterparties, there is a risk of receiving a cancelled payment or a fake confirmation.

Solution – only use verified P2P platforms with escrow, check user ratings, and do not hand over crypto until you have received actual confirmation of payment.

Checklist: a secure off-ramp in 7 steps

- Choose a method that suits your volume, region and frequency of transactions.

- Use stablecoins to lock in the exchange rate before the final withdrawal.

- Check all fees (including hidden ones!) – trading, withdrawal, conversion and incoming payments.

- Take account of taxes in your jurisdiction – keep track of costs and dates.

- Diversify your withdrawal channels – don’t put all your eggs in one basket.

- Test with small amounts before carrying out large transactions.

- Automate via API where possible to minimise human error and delays.

How 0xProcessing simplifies withdrawals for businesses

0xProcessing offers a comprehensive crypto-to-bank-account solution that combines all stages of working with cryptocurrency: accepting customer payments in 65+ currencies, automatic conversion via VRCS (volatility protection), fund consolidation and flexible withdrawal options.

Our infrastructure allows you to set up a fiat off-ramp to your account in euros or dollars and integrate via a simple API. Find out more about withdrawal options with 0xProcessing.

Conclusion and findings

An effective off-ramp in 2026 is not simply a matter of finding an exchange with low fees. It is a comprehensive strategy that includes:

- Using stablecoins as a universal bridge to lock in exchange rates and move funds quickly between platforms.

- Diversifying withdrawal channels – a combination of exchanges for large sums, P2P for regions with restrictions, and professional payment gateways for regular transactions.

- Taking regional specifics into account – SEPA Instant and virtual IBANs operate in Europe, zero capital gains tax in Asia and the UAE, and complex regulation in the US.

- Automation via API – manual withdrawals from a dozen exchanges are not scalable for a growing business.

- Risk management – diversification of platforms, working only with trusted partners, full compliance.

Don’t look for "one perfect method" – build a system from several channels suited to your volumes, regions and types of transactions. Start small, test and scale what works.

Frequently asked questions about off-ramps

What is the cheapest way to convert crypto to fiat?

The cheapest method depends on the amount and region. P2P platforms are effective for small amounts. Payment gateways are optimal for regular business with higher volumes.

How long does it take to withdraw crypto to a bank account?

Via centralised exchanges – 1–3 working days. Via P2P – from a few hours to several days, depending on the counterparty. Via modern payment gateways using stablecoins – minutes.

What are the best stablecoins for off-ramping?

USDT (Tether) – highest liquidity, available on all platforms, across multiple networks (ERC-20, TRC-20, BEP-20, Solana). USDC (Circle) – more regulatory transparent, particularly in Europe (complies with MiCA), preferred for institutional transactions.

Can I withdraw crypto directly to my business bank account?

Not directly – you need an intermediary (exchange, payment gateway, licensed provider) that will accept the cryptocurrency, convert it to fiat and send it via SWIFT/SEPA/ACH transfer to your account. There are no direct transfers from the blockchain to a bank account.

How to choose an off-ramp partner for large volumes?

Look out for: regulatory status (licences), partner network of banks, withdrawal speed, transparency of fees, availability of an API for automation, market reputation and feedback from other institutional clients.